![]()

")

")

Why rubber prices have plunged

The recent fall in natural rubber prices has attracted wide attention of the media and hectic parleys between the stakeholders and the concerned authorities. The monthly average price of RSS-4 grade (the most popular form of rubber processed in the country) fell from a peak of ₹238.68 /kg in April 2011 to ₹152.69 in January.

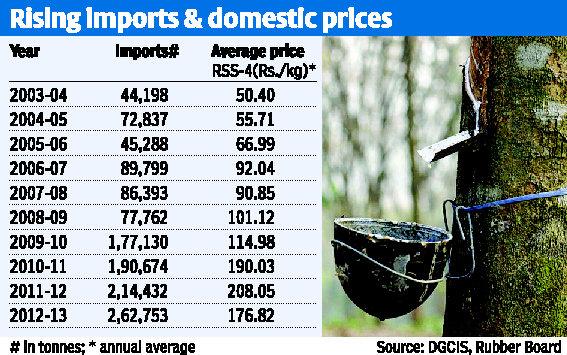

Volume of imports

In popular parlance, the role of steady increase in rubber imports has been considered pivotal in prompting the downtrend in prices. In fact, the volume of imports has registered a three-fold increase from 77,762 tonnes in 2008-09 to 2,62,753 tonnes in 2012-13. In the current financial year, the volume of imports is fast approaching the three-lakh-tonne-mark. In this process, the import intensity of the domestic rubber consumption has reached an unprecedented level of 27.01 per cent in 2012-13. Hence, it is logical to link the fall in prices to the surge in imports and the need for explicit policy measures to replenish market sentiments.

However, trends in the volume of imports and domestic prices during the last decade are not only a negation of the perceived inverse relationship between the two variables but also revealed a positive correlation(r=0.91). The table provides details.

The hypothesis of cheaper imports leading to fall in prices is unconvincing and masks the underlying factors from the purview of any systematic analysis. This obsession conveniently overlooks two recent trends — the channel and cost of imported rubber. Since 2010-11, there has been a steady increase in imports through the duty paid route, with the share of rubber imports through the duty paid channel rising from 7.01 per cent in 2004-05 to 47.33 per cent in 2012-13. Therefore, it is plausible to presume that the growth in imports through duty paid channel has been either due to comparative cost advantages or supply side rigidities.

Why rubber prices have plunged

Tyre sector

Interestingly, the annual average cost of the major form of imported rubber (TSR-20 grade) through duty paid route was higher than the annual average domestic prices of comparable grades in India during 2011-12 and 2012-13. The tyre sector accounted for over 97 per cent of the imports through duty paid route.

Technically, the extent of burden of higher unit value of imports on the tyre sector depends on its capability to shift the same in the form of higher product prices to consumers. In this context, the observations on the pricing policy of the tyre sector contained in the Report of the Competition Commission of India (2012) deserve attention. On the other side, the annual growth rate in tyre imports was 38.68 per cent compared with 18.37 per cent in exports during the last one decade. In sum, chances of higher volumes of imports through duty paid route with higher costs loom large in the backdrop of the expansion of the domestic tyre market.

Apparently, emerging trends are indicative of the supply side rigidities in feeding the growing consumption requirements of the tyre sector.

In this context, two aspects deserve attention — the determinants of domestic price and policy proposals to address the current imbroglio. As said earlier, domestic price movements have been increasingly determined by global market prices since 1992 compared to the domestic supply and demand as well as policies on imports during 1947-91.

The removal of quantitative restrictions on imports since March 31, 2001, has accelerated the market integration process and price determining mechanisms. The most discernible outcome of the process has been the transmission of perennial uncertainty in world market to the domestic market.

Therefore, the basic issue is the potential implications of instability in rubber prices and the policy approaches to address it. The validity of this proposition is underlined by the inherent limitations of the policy measures pursued during 1997-2001 in addressing the fall in domestic prices.

The five policy measures (spelt in the above box) could not achieve the perceived objectives and prices realised by the planting community have been in tune with global price movements rather than the statutory minimum prices.

The explicit inputs from the cumulative outcomes of the five policy measures assume relevance in the current scenario as the proposed initiatives closely resemble the five policy measures. Conceptually, the futility of the measures is closely related to a pre-reforms mindset surrounded by tariff walls and non-tariff barriers. Unfortunately, instabilities in the commodity prices have been an outcome of the growing financialisation of commodity markets since 2002.

Hence, unlike in the pre-reforms phase the domestic price stabilisation measures have serious limitations when financial investors dominate commodity markets. In the changed scenario, a comprehensive crop insurance scheme covering crop and income losses would be a better option.

The author is Joint Director, Rubber Research Institute of India. The views are personal

http://globalrubbermarkets.com/16640/rubber-prices-plunged.html

Contact :

Tel : +66 2 582 3003